Asset Class: Gold & Bullion

Loans Against Gold and Bullion

Discreet lending of £61,000 to £2,000,000 secured against investment-grade bullion, coins and high-purity jewellery, exclusively for certified high-net-worth individuals.

Who this is for

Liquidity against the gold you already own

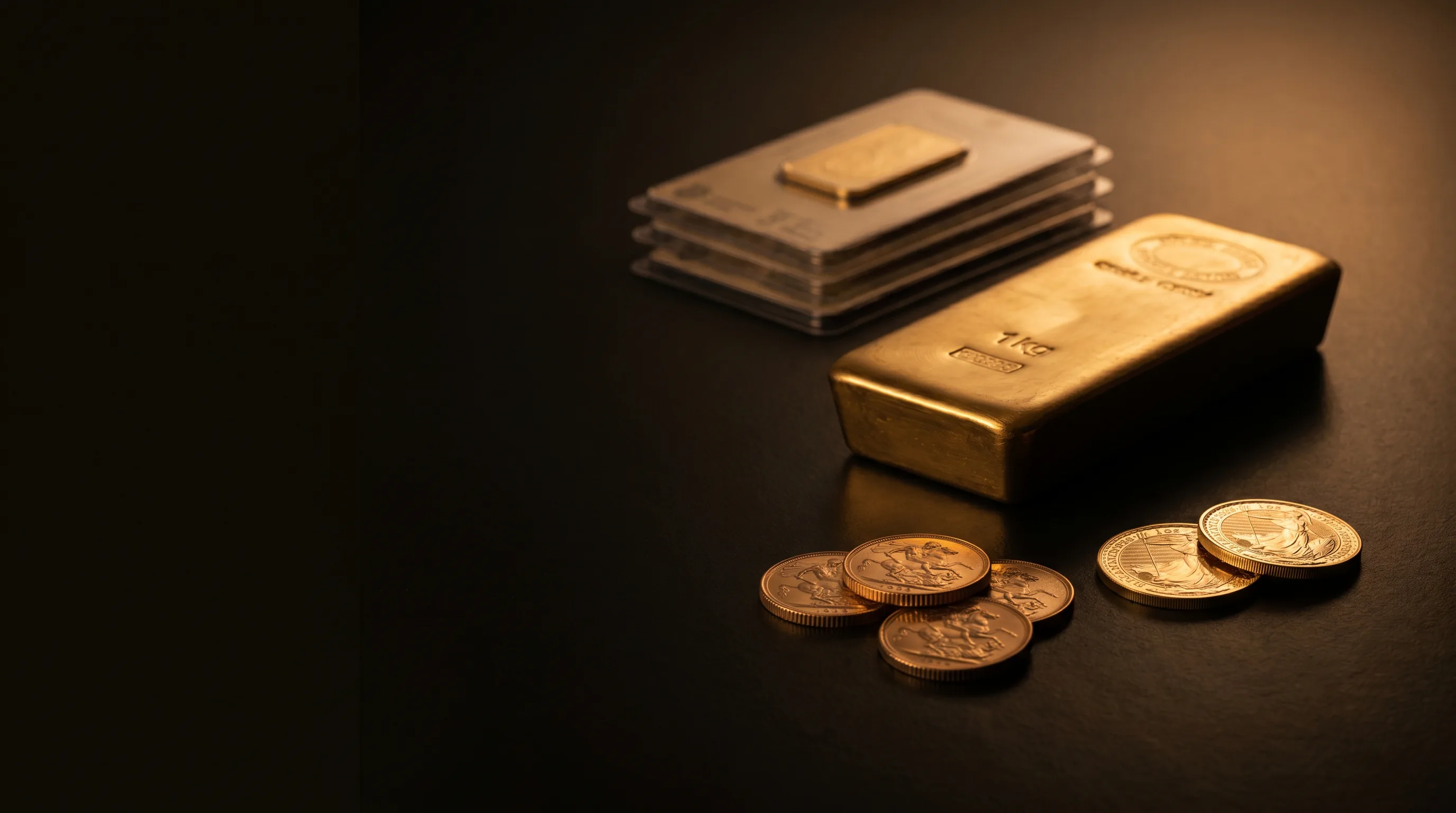

SAFE Lending Co provides direct gold loans across the UK, secured against investment-grade bullion, hallmarked jewellery, Sovereigns, Britannias, Krugerrands and high-value numismatic coins. Loans start at £61,000 and scale to £2,000,000, with terms of 3 to 12 months and no early repayment fees after the initial 3-month period.

Our clients are typically asset-rich individuals who want to unlock liquidity without selling: to bridge a property transaction, settle a tax bill, fund a business opportunity, or cover a probate timing gap. The gold stays in our allocated, insured vault. You retain ownership and any market upside in the gold price.

Roughly 85% of pawnbroking clients redeem their assets at the end of the term. Most never intended to sell their gold; they simply needed liquidity for a short window. Our service is built around that outcome.

What we lend against

Five categories of gold are accepted as collateral, each valued on its own merits: bullion content first, with collector premium where it exists.

Investment-grade bullion bars

PAMP Suisse, Royal Mint, Argor-Heraeus, Umicore, Valcambi and other LBMA Good Delivery refiners. From 1 oz to 1 kg bars and larger.

Sovereigns, Britannias & Krugerrands

Full Sovereigns, Half Sovereigns, Britannia 1 oz coins, South African Krugerrands and other recognised investment coins.

9ct to 24ct jewellery

Hallmarked jewellery in any purity from 9 carat to 24 carat. Chains, rings, bracelets, watches and ceremonial pieces.

Numismatic and collector coins

Rare and graded coins where collector premium materially exceeds bullion value: Edward VII Sovereigns, proof sets, historic strikes.

Heritage and ceremonial gold

Tableware, ceremonial regalia, antique gold artefacts. Provenance and hallmarks help establish a premium over scrap value.

Inherited and probate gold

Gold held through an estate or probate where you need liquidity ahead of distribution. A loan against the gold avoids a forced sale and the CGT implications a disposal may carry while the estate is being settled.

Valuation

How your gold is valued

Every valuation is built on the live LBMA spot price, confirmed purity from non-destructive testing, and a premium for any provenance or collector interest the piece carries.

Live LBMA spot reference

We benchmark every valuation against the twice-daily LBMA Gold Price in pounds sterling per troy ounce. You see the exact spot reference used in your valuation, not a static figure.

Non-destructive purity testing

XRF spectrometry confirms purity without damaging the asset. We do not scratch, file or cut. Hallmarks from the London, Birmingham, Sheffield and Edinburgh assay offices are cross-checked against UK records.

Premium over spot, where it exists

Collector coins, signed pieces, original boxes and historic provenance attract a premium over scrap. Our auction-house-trained valuers identify value above metal content.

Storage

How your gold is stored

For the duration of the loan, your gold sits in an allocated, insured, climate-controlled vault, inspectable on request.

Allocated, fully insured vault

Your gold is stored under your name in a climate-controlled vault. Allocated means your specific items are set aside, not pooled with other clients' holdings.

Audited and inspectable

Storage locations are independently audited. You may inspect your gold during the loan with 48–72 hours' notice. Chain-of-custody documentation is available on request.

Insured nationwide collection

Door-to-door insured collection across the UK by trained handlers. Our team is insured to handle assets up to £5,000,000 in value.

Pawn or sell?

Selling realises today. Pawning keeps you in the asset.

Selling your gold ends your position in it. A loan secured against the same asset gives you the cash you need and leaves the upside in your hands. For most of our clients, particularly those whose need is for short-term liquidity rather than permanent divestment, the maths favours pawning.

Selling investment-grade bullion may trigger Capital Gains Tax. UK legal-tender coins (Sovereigns and Britannias) are CGT-exempt for UK residents; other bullion is not.

A loan secured against your gold is not a disposal, so no CGT event arises.

You retain any market upside in the gold price during the loan period.

85–88% of pawnbroking clients redeem their assets at the end of the term. Most never intended to sell.

This is general information, not tax advice. Speak to a qualified tax adviser or visit HMRC for guidance specific to your circumstances.

Related reading

Guides to help you weigh up borrowing against your assets.

Gold Lending: Common Questions

Answers to the questions we hear most often from clients borrowing against gold.

In legal terms, yes: a loan secured against gold with the asset held by the lender is pawnbroking. We use the term "asset-backed lending" because our service is built around high-value clients and discreet, specialist valuation rather than the high-street pawn experience. The mechanics are identical: you receive a loan, we hold the gold securely for the term, you repay and recover the asset, or, in the rare case of non-repayment, the gold is sold and any surplus above the outstanding balance is returned to you.

Investment-grade bullion bars from LBMA Good Delivery refiners (PAMP, Royal Mint, Argor-Heraeus, Umicore, Valcambi and others), Sovereigns and Britannias, Krugerrands, hallmarked jewellery from 9 carat to 24 carat, numismatic and collector coins, antique or ceremonial gold pieces, and gold held through estates or probate. Minimum total value £61,000.

We benchmark against the twice-daily LBMA Gold Price in pounds sterling and confirm purity using non-destructive XRF spectrometry. For collector coins, signed pieces and historic provenance, our auction-house-trained valuers assess any premium above the bullion value. You see the spot reference used and the components of the valuation.

Yes. Purity is confirmed by XRF testing regardless of hallmark. Hallmarks help speed up the process and may support a higher valuation on antique or branded pieces, but they are not a requirement.

9 carat gold is 37.5% pure; 24 carat is 99.9% pure. Loan value scales with purity by mass, so 1 gram of 24ct is worth approximately 2.7 times 1 gram of 9ct at the same spot price. We test every item to confirm actual purity rather than relying on stamps.

Yes. They typically carry a small premium over their gold content because of collector demand and their status as UK legal tender. We assess each coin individually and reflect any condition or rarity premium in the valuation.

In allocated, climate-controlled, fully insured vault storage. Allocated means your specific items are set aside in your name, not pooled with other clients' holdings. You may inspect your gold during the loan with 48–72 hours' notice. Chain-of-custody documentation is available on request.

Yes. Storage is fully insured and our handling team is insured to manage assets up to £5,000,000 in value. Cover is in place from the moment we take possession through to redemption or sale.

A loan secured against your gold is not a disposal and does not trigger Capital Gains Tax. Selling investment-grade bullion may trigger CGT, although UK legal-tender coins (Sovereigns and Britannias) are CGT-exempt for UK residents. This is general information, not tax advice. Please consult a qualified tax adviser for your specific circumstances.

Yes. After the minimum 3-month term, you can redeem your gold at any time with no early repayment fees or exit charges. Simply repay the outstanding loan balance and accrued interest.

We always work with clients to explore extension options before this point. If the loan is not repaid by the end of the agreed term, the gold may be sold to recover the debt. Any surplus funds from the sale above the outstanding balance are returned to you.

Ready to discuss a loan against your gold?

Submit an enquiry with a few details about the asset. We respond within 24 hours and arrange a free valuation. No commitment, no fee.